App Store

App Store Profile

Profile Security

Security Sign Out

Sign Out

Feeds

Feeds

Articles

ArticlesWhere Did FTX’s $138 Billion Go? The Shocking Math Behind the Bankruptcy

FTX: Where Did the Money Go — And Who Took Control

When FTX collapsed in November 2022, over seven million users had deposited roughly $20 billion. The exchange froze withdrawals and filed for bankruptcy, leaving an $8 billion customer hole. For years, creditors waited—until 2025, when the estate announced full repayments of 119-143% of claims.

Ironically, the company was never truly insolvent; it suffered a liquidity crisis, not a balance-sheet failure.

The Missed Path

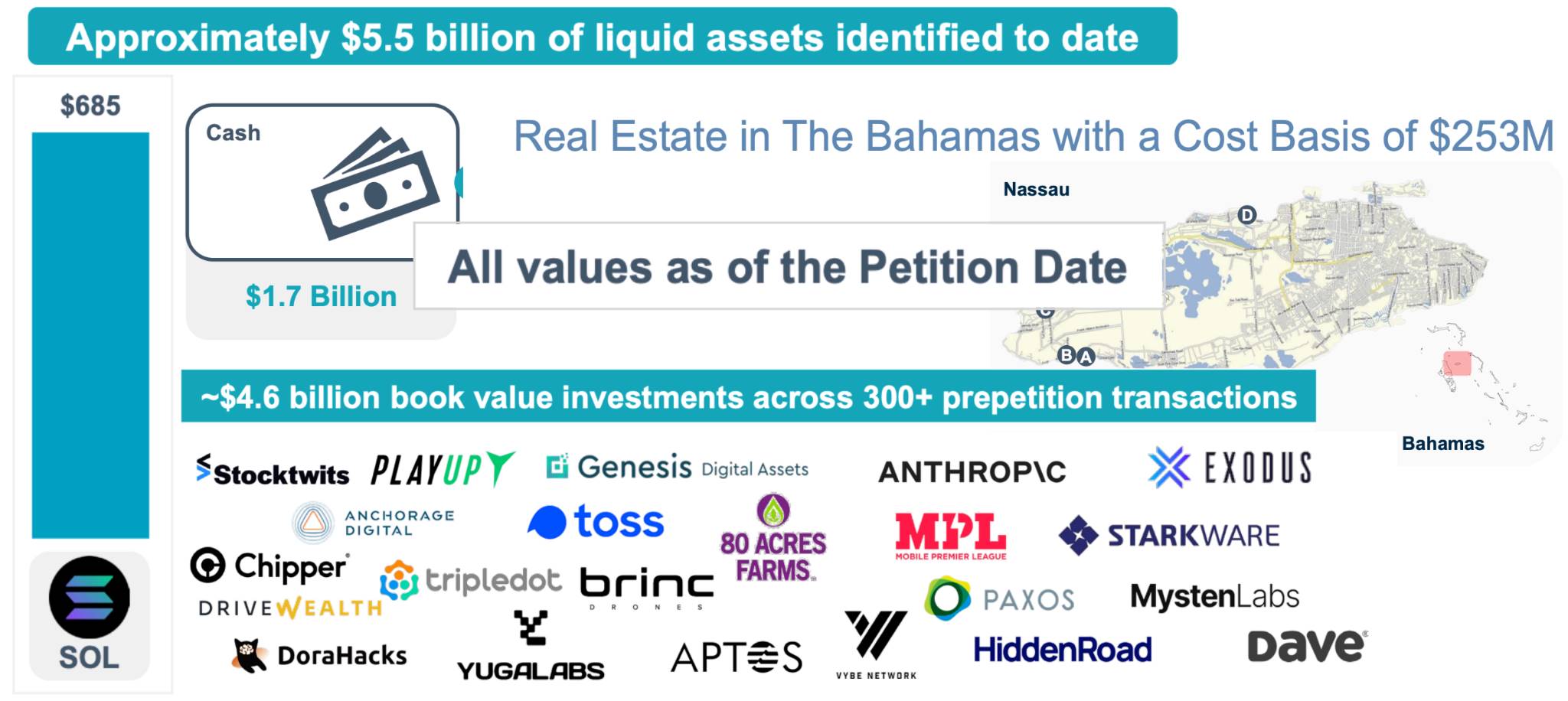

Court filings show that as of the bankruptcy date, FTX still held $14.6 billion in assets—enough to repay users in-kind.

These included:

$5.5 B in cash & liquid crypto

$4.6 B in venture investments

$3.7 B in illiquid tokens

Real estate + subsidiaries worth ≈ $0.4 B

Had withdrawals resumed and assets not been seized, customers could have been made whole by late 2022.

By September 2025 valuations, those same holdings would exceed $136 billion—with massive exposure to winners like Anthropic ($14.3 B), Solana ($12.4 B), FTT ($21.9 B), and Robinhood ($7.6 B). In short, the estate that’s now distributing ~$18 B could have been worth nearly eight times that.

What Went Wrong

According to the document, once external counsel Sullivan & Cromwell (S&C) and attorney John J. Ray III took control on Nov 11 2022, the company was placed into a Delaware bankruptcy—despite FTX still processing withdrawals and negotiating liquidity deals.

Within hours, the exchange was shut down, staff fired, and S&C retained as bankruptcy counsel.

The report alleges that these lawyers had incentives to push for bankruptcy because fees would then be paid directly from the estate.

To date, nearly $950 million in legal and consulting fees have been approved, with another $450 million reserved—making the FTX case one of the costliest since Lehman.

Narrative Control

Publicly, Ray and S&C portrayed FTX as “hopelessly insolvent,” using early statements that allegedly misrepresented its balance sheet.

Prosecutors in Sam Bankman-Fried’s trial echoed that framing, citing liabilities while ignoring offsetting assets.

Documents show that even in 2022, Alameda and FTX together held $25 B in assets against $13 B in liabilities, remaining solvent on paper.

The report suggests that calling it a “dumpster fire” justified shutting down operations and liquidating holdings at depressed prices—often to insiders or below market value.

Value Erosion

If Ray’s team had simply frozen operations and waited, the estate might now hold $136 B in assets and $111 B in net value. Instead, after sales, fees, and settlements, less than $18 B remains.

Key losses cited:

FTX Equity: $66.4 B

FTT Token: $21.9 B

Anthropic Stake: $12.9 B

Solana: $9.1 B

Robinhood: $7.0 B

Sui: $2.8 B

Legal & Consultancy Fees: $1.4 B

Government Claims & Settlements: $16.9 B

Total Losses ≈ $138 B of value destroyed

The Core Argument

The 25-page document—authored by Sam Bankman-Fried and team—asserts that FTX was solvent throughout, and that its collapse was worsened by the lawyers’ intervention, asset fire sales, and self-serving incentives.

Critics note that this framing may absolve FTX leadership of negligence, yet the underlying math shows something undeniable: the assets were real, the prices recovered, and the bankruptcy process itself may have consumed most of the potential upside.

Today

Customers are finally being repaid—but in USD, not crypto. A user owed 1 BTC in 2022 will receive ~$17 K, even though Bitcoin now trades near $114 K. Equity investors who put in $1.95 B get back ~$230 M.

So yes, everyone’s “made whole,” but only in a narrow legal sense. In real terms, the FTX estate may have burned over $120 B in potential value.

Source

Source

Add to Favorites

Add to Favorites Download image

Download image Share x

Share x Copy link

Copy linkBitcoin may enter a prolonged sideways phase between $57K and $87K as markets enter a relief period following a 52% drop from ATH. This consolidation could mirror the 2022 fractal, creating liquidity before a potential breakdown toward the $44K–$50K range.

Doctor Profit/2026.03.09

Davinci Jeremie urged people to buy $1 of Bitcoin in 2013 and became a symbol of early conviction. Years later, fame, lifestyle flexing, and token promotions sparked criticism. His journey reflects both crypto foresight and influencer-era controversy.

StarPlatinum/2026.03.04

A sweeping narrative ties Jane Street to India’s expiry-day options case, alleged 10AM Bitcoin sell patterns, Terra’s collapse, and ETF plumbing. While none prove misconduct, critics argue a common structure: move spot, monetize derivatives, keep execution opaque.

Bull Theory/2026.02.27

A controversial narrative links Jane Street, ETF mechanics, and Bitcoin’s price behavior, pointing to lawsuit allegations, 10AM volatility patterns, and derivative hedging dynamics. The discussion raises broader questions about liquidity, structure, and price discovery.

Justin Bechler/2026.02.26

A new federal lawsuit alleges Jane Street exploited non-public information tied to Terraform’s liquidity defenses, accelerating UST’s depeg and the Terra collapse. The firm denies the claims. The case may reignite debates on structure, design, and regulation.

Diana/2026.02.25

Mean reversion and on-chain models sit at levels historically linked to bottom formation after capitulation. Realized losses reached record USD values, while deviations from anchor models remain extreme. Price pain may be fading; patience remains key.

Checkmate/2026.02.25

Hot feeds

A trader profits $448K by monitoring #Binance's new listings!

2024.12.13 17:37:29

Last week, funds have flowed into #Bitcoin, #Ethereum, and #Hyperliquid.

2024.12.16 14:48:36

A $PEPE whale that had been dormant for 600 days transferred all 2.1T $PEPE($52M) to a new address.

2024.12.14 10:35:27

When Elon Musk tweeted about Moltbook, the meme coin MOLT experienced a short-term 30% price surge, hitting a new all-time high of $114 million.

2026.01.31 18:37:29

A smart #AI coin trader made $17.6M on $GOAT, $ai16z, $Fartcoin,$arc.

2025.01.05 16:05:18

A sniper earned 2,277 $ETH ($8.3M) trading $SHIRO within 18 hours!

2024.12.03 23:09:08

MoreHot Articles

How did I turn $1,000 into $30,000 with smart money?

2024.12.09

10 promising AI Agent cryptos

2024.12.05

The 30-Year-Old Entrepreneur Behind Virtual, a Multi-Million Dollar AI Agent Society

2025.01.22

10 smart traders specializing in MEMEcoin trading on Solana

2024.12.09

A trader lost $73.9K trading memecoins in just 3 minutes — a lesson for us all!

2024.12.13

What is $SPORE? Let us take you through the on-chain records to show you how it works.

2024.12.25